Tax rules are changing again in 2026. While that might sound overwhelming, we’ve broken it down into six key updates that could affect your wallet, your savings and your giving plans.

Jump ahead:

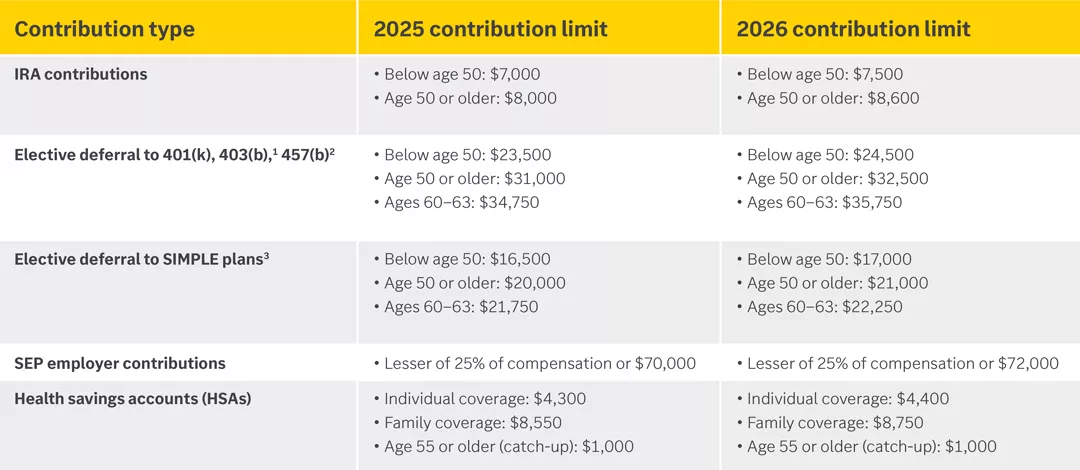

1. Contribution limits increased

2. New catch-up contribution rule for high-income earners

3. Higher 529 account distribution limits for K-12 expenses

4. Trump accounts available through the Treasury

5. A charitable contribution deduction for nonitemizers and a new floor for itemizers

6. New limit on total itemized deductions for those in the 37% bracket

1. Contribution limits increased

The IRS typically increases contribution amounts on an annual basis. This means the new year rings in opportunities to save even more on a tax-advantaged basis for retirement and health care.

1 Additional service-based catch-up contributions may be permitted. Consult your plan administrator.

2 Limit applies to combined employee and employer contributions.

3 Certain plans can contribute 110% of contribution limits. Consult your plan administrator.

Actions to consider: The new year’s a good time to review your contributions to ensure you’re saving enough to meet your goals. If you’re not quite there or you just want additional cushion for your strategy, try to increase your contributions this year by an amount that’s comfortable for you — even small amounts can add up over time. Consider making your increases automatic if that option’s available to you.

If you’re still working on your 2025 taxes, you can make contributions to IRA and HSA accounts until April 15, 2026. SEP IRA contributions (for business owners and self-employed individuals) can be made through your tax-filing deadline, including extensions.

2. New catch-up contribution rule for high-income earners

If you’re age 50 or older and your wages exceeded $150,000 last year, you’ll only be able to make Roth catch-up contributions in your workplace retirement plan this year. This includes 401(k), 403(b) and 457(b) plans.

Actions to consider: While you may not get a tax benefit from your plan catch-up contributions this year, you should generally still make them if you originally planned to. Roth contributions offer the potential for tax-free income in retirement and a tax-free legacy for your heirs. You won’t get those benefits elsewhere.

3. Higher 529 account distribution limits for K-12 expenses

The annual federal limit on 529 plan distributions for qualifying K-12 expenses doubles in 2026 from $10,000 to $20,000 per student. Plus, more types of K-12 expenses now qualify for tax-free withdrawals since the definition expanded last year to include curriculum, books, certain tutoring expenses and certain testing fees, among others.

Actions to consider: If you want to use your 529 to cover K-12 expenses, consider making additional contributions to take advantage of tax-free earnings growth. In 2026, you can make a $19,000 gift per donee ($38,000 if you're married and eligible to gift-split) without using your federal estate and gift tax exemption. You can also elect to contribute up to five years’ worth of the annual exclusion in a single year without using your exemption, subject to special 529 savings plan rules. Some states may also allow tax-free withdrawals for K-12 expenses and provide a state income tax deduction for contributions to the plan.

If you have an overfunded 529 plan, the higher limit and expanded definition for K-12 expenses increases the flexibility for excess funds. You can change the beneficiary to an eligible family member of the original beneficiary to help cover their K-12 costs.

4. Trump accounts available through the Treasury

Starting in July 2026, you can open and fund Trump accounts through the Treasury. Trump accounts are “starter” IRAs for children with special rules until age 18, including nondeductible contributions up to $5,000 (which don’t count toward normal IRA limits or require taxable compensation), limited investment options and no distributions until age 18. Additionally, children born between 2025 and 2028 will be granted a one-time contribution of $1,000 from the federal government, which doesn’t count toward the annual contribution limit.

Actions to consider: If your child was born in 2025 or 2026, be sure to open a new Trump account for them to receive the one-time free $1,000 contribution. For any child under age 18, consider contributing to an account if you’re on track for your own retirement, helping fund your child or grandchild’s retirement is one of your goals, and the child doesn’t have taxable compensation or is already maxing out their IRA. This can be a great way to give your child or grandchild a head start on their retirement savings.

5. A charitable contribution deduction for nonitemizers and a new floor for itemizers

There are two new charitable deduction provisions in 2026, and their impact depends on the type of deduction you take on your tax return:

- For those who take the standard deduction, you’re now allowed a deduction for cash charitable contributions of up to $1,000 ($2,000 if filing jointly). These donations must be made to a qualified charitable organization, which excludes donor-advised funds (DAFs).

- For those who itemize their deductions, only your charitable contributions that exceed 0.5% of your adjusted gross income (AGI) are now deductible.

Actions to consider: If you take the standard deduction, you can now receive a tax benefit for your contributions, allowing you to reduce your taxes while fulfilling your charitable goals. Be sure to keep good records of your cash donations.

If you itemize deductions, consider bunching strategies or using a DAF to help reduce the floor’s impact, especially if you typically donate less than 0.5% of your AGI. Even better, if you’re 70½ or older and taking required minimum distributions (RMDs), consider making your donations directly from your IRA through a qualified charitable distribution (QCD). You’ll receive the full benefit of your donation and reduce your AGI since QCDs satisfy your RMD.

6. New limit on total itemized deductions for those in the 37% bracket

If you’re in the 37% federal marginal tax bracket, the tax benefit of your itemized deductions will be limited to 35% starting in 2026. This limitation applies after any applicable deduction-specific limits such as the charitable contribution deduction AGI floor mentioned above.

Actions to consider: If the new rule affects you, explore strategies that reduce your AGI and align with your goals to help offset the impact of disallowed itemized deductions. Some ways to do this include making additional contributions to your HSA, pretax contributions to your workplace retirement plan (if you’re comfortable with forgoing the potential for tax-free growth with Roth contributions), QCDs or tax-loss harvesting if you have positions with losses. You may also need to set aside additional money for taxes this year or make higher quarterly payments.

Several TCJA provisions have been indefinitely extended

In addition to the above changes, many provisions of the Tax Cuts and Jobs Act (TCJA) that were set to expire after 2025 have been indefinitely extended, including but not limited to: the lower individual income tax rates, the higher standard deduction, the elimination of personal exemptions, the higher alternative minimum tax exemption and phaseouts, the qualified business income deduction and the higher estate tax exemption.

We're here to help

Navigating these tax changes can be challenging, but you don’t have to navigate them alone. Your financial advisor and tax professional can help you further understand how you might be impacted. Since this list isn’t exhaustive, be sure to ask about additional changes that might affect your unique tax situation.

This content is provided for educational purposes only and should not be interpreted as specific investment, tax or legal advice. While the information is believed to be accurate, it is not guaranteed and is subject to change without notice.

Edward Jones, its employees and financial advisors cannot provide tax or legal advice. You should consult your attorney or qualified tax advisor regarding your situation.